TLDR:

- Customer experience in banking is now benchmarked against every digital interaction, not just other financial services providers.

- Switching is rarely about price. Friction, poor communication, and one badly handled moment are the real drivers of customer defection.

- Claims handling in insurance and channel handoffs in banking are the two highest-impact CX problems to fix first.

- A structured Voice of the Customer program is what separates organisations that react to complaints from those that prevent them.

- NPS matters, but only as one signal among several, and the direction of change over time tells a more useful story than any single score.

Customer experience in banking is no longer a soft advantage. It is a commercial imperative, and most financial services organisations are still playing catch-up. According to PwC’s Experience is Everything report, 32% of customers will walk away from a brand they love after just one bad experience. In a sector where trust takes years to build and minutes to lose, that is not a stat to sit with comfortably.

This article covers the biggest CX gaps in banking and insurance, how to build a Voice of the Customer (VoC) program that actually changes operational behaviour, and what good looks like when it comes to measuring CX performance in financial services.

Why Customer Experience in Financial Services Is a Business-Critical Problem

Here is the uncomfortable truth: financial services companies spent decades assuming that switching barriers were a substitute for loyalty. They were not. They just delayed the moment customers left.

How One Bad Interaction Ends a Ten-Year Relationship

Trust in financial services is built slowly and lost fast. A customer can spend a decade with the same bank, never miss a payment, and walk away after one interaction where they felt ignored, misled, or passed around to the fourth person who still did not have their details.

The relationship does not protect them from a bad experience. Often it makes the disappointment worse because the expectation was higher.

What Rising Customer Expectations in Banking and Insurance Actually Look Like

Customers do not always complain when something goes wrong – they just leave. Research by Bain & Company consistently shows that switchers in banking rarely cite price as the main reason for leaving. They cite friction, feeling unheard, or one interaction that went badly at the wrong moment.

The expectation shift is structural. Customers now benchmark their bank against every digital experience they have, not just other banks and insurers. The standard was set by companies that built four-minute onboarding flows and proactive push notifications. Financial services is measured against that benchmark whether it wants to be or not.

How Fintech Challengers Reset the CX Benchmark

Leading challengers did not win customers on rates. They won on clarity and speed. Instant notifications, clean interfaces, frictionless account opening. These are not premium features anymore. They are baseline expectations. Incumbents that treat them as nice-to-haves are operating with a growing experience deficit.

The fintech effect has also compressed tolerance. A generation of customers who have never walked into a branch does not have the same patience for friction. For them, making a payment in two taps is normal. Waiting on hold for 20 minutes is not.

Why Financial Services Still Lags Other Industries on CX

Legacy infrastructure is part of it. Risk aversion in regulated environments is part of it. But a lot of it comes down to the fact that switching barriers kept customers in place long enough that CX investment did not feel urgent. Open banking, embedded finance, and better alternatives have changed that calculation entirely.

According to McKinsey, financial services firms that lead on personalisation and CX generate up to 20% higher customer satisfaction rates and significantly stronger revenue growth over time. The investment case is there. The urgency is building.

CX Guides | free to download

No fluff. Just CX strategy guides for real-world use. Get tips from the experts.

The Biggest CX Gaps in Banking and Insurance

The gaps are not hard to find. They show up in complaint volumes, in call centre queues, and at the moment a customer has to repeat their account details to the fourth person they have spoken to. Most of these problems are known. The ones that move the needle most share a common characteristic: they are operational, not aspirational.

How to Improve Customer Experience in Banking

Fixing the Channel Handoff: Where Banking CX Most Visibly Breaks Down

The channel handoff is where customer experience in banking most visibly falls apart. A customer starts an application online, calls a branch to ask a question, and the branch has no record of it. They start again. From scratch.

The fix is not complicated: shared customer data, consistent records across touchpoints, and a single view of the customer journey. Most banks know this. Far fewer have implemented it end to end. The gap between knowing and doing is where CX programmes stall.

The High-Impact Moves That Shift the Dial Fastest in Retail Banking

Proactive communication is one of the highest-return investments a retail bank can make. Alerting a customer before a direct debit fails, or flagging a potential fraud attempt before they notice it, reduces inbound contacts and builds trust simultaneously. You are solving the problem before they knew they had one.

First-contact complaint resolution is the other lever. Financial services firms that resolve complaints without escalation consistently show lower overall complaint volumes and higher NPS. Every escalation is a signal that something upstream failed. Tracking escalation rates by product and branch tells you exactly where to fix it.

How to Improve Customer Experience in Insurance

Why the Claims Moment Defines the Entire Customer Relationship

Claims is where the product has to actually work. A customer filing after a flood or a vehicle accident is stressed, often out of pocket, and paying close attention to everything you do. That interaction determines whether they renew. Whether they recommend you. Whether they stay.

The organisations that get this right do not treat claims as a cost centre. They treat it as the most important CX moment in the entire insurance relationship. How a claim is handled in the first 48 hours shapes how the customer remembers the insurer for the next 48 months.

What Leading Insurers Do Differently in CX Management

They build their CX strategy around claims rather than acquisition. They measure settlement speed, follow up after claims close, and train handlers to communicate clearly under pressure. Empathy training and plain-English correspondence are not soft investments. They show up directly in NPS and renewal data.

The best insurers also close the loop. When a customer’s claims experience generates a low satisfaction score, it triggers a follow-up. Not a form, but a conversation. That is the difference between collecting feedback and acting on it.

Building a Voice of the Customer Program for Financial Services

Most financial services companies collect some form of customer feedback. A proper Voice of the Customer program is different. It captures insights at defined points in the journey, maps them to specific products and interactions, and routes them to the teams who can actually act on them.

What a Real VoC Program Looks Like in Financial Services

The Difference Between a Feedback Form and a Structured VoC Program

A feedback form captures self-selected opinions, usually from customers who are either very happy or very frustrated.

A VoC program captures structured insights across the full customer base, at the moments that matter most, and ties them to operational outcomes rather than just reporting scores. It tells you what is driving your NPS. It tells you which branch, which product, which interaction type is generating the most friction. And it gives your teams something actionable to work with instead of a number to report upward.

Key Benefits of a VoC Program in Regulated Industries

In regulated industries, VoC data does double duty. It improves CX and it surfaces risk early. Complaint patterns and service failures that might otherwise reach a regulator can be caught and resolved internally when the right feedback infrastructure is in place.

This is increasingly relevant. Regulators across the UK, Australia, and the US are paying closer attention to how financial services organisations treat customers. A strong VoC program is both a CX tool and a risk management asset.

How to Turn VoC Data Into Operational Change

Connecting Customer Feedback to Frontline Behaviour

The insights are only useful if they change something. The organisations that get the most out of VoC programs give team leaders feedback on their own teams, not just company-wide averages. They set quarterly priorities directly from the data. They have a defined process for escalating systemic issues, rather than letting them accumulate in a dashboard that nobody opens.

Robyn AI, the AI engine within Resonate CX, surfaces the themes underneath the scores automatically, telling you not just that NPS dropped, but which interaction types and friction points are driving it. No data analyst required. No three-week reporting cycle. The insight is there when you need it.

Measuring CX in Financial Services: NPS, CES, and What Good Actually Looks Like

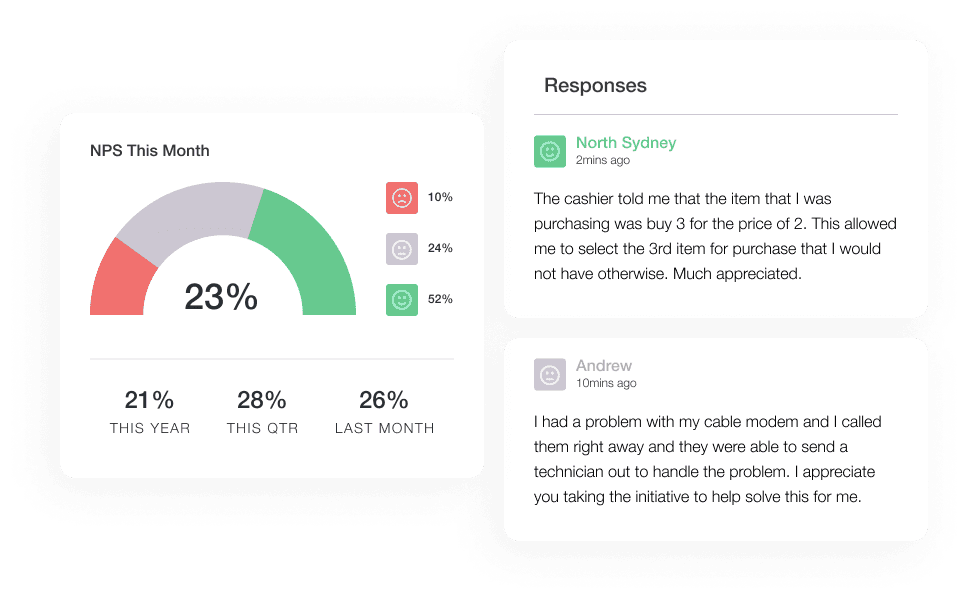

Net Promoter Score is the most common CX metric in financial services, but it works best as one signal among several. Used alongside complaint data, customer effort scores (CES), and operational metrics, it tells a useful story. Used alone, it is slow to diagnose and easy to game.

What Is a Good NPS Score for Financial Services?

Retail banking tends to score lower than most people expect. Industry benchmarks from Bain & Company place average retail banking NPS in the range of 20–35 for major incumbents, well below sectors like streaming or e-commerce. Insurance typically scores lower still, and is heavily influenced by whether the customer has recently made a claim. Wealth management tends to sit higher, partly because client relationships are more personal and more frequent.

Across all three, the direction of change over time matters more than any single score. A firm moving steadily upward is doing something right, even if the number looks modest against a fintech challenger. A high NPS that is declining is worth worrying about more than a modest NPS that is improving.

Resonate CX’s CX Benchmarking capability lets financial services organisations compare their NPS and satisfaction scores against industry peers so you know not just whether you are improving, but whether that improvement is keeping pace with the market.

How Resonate CX Helps Financial Services Organisations Manage and Improve CX

Financial services teams do not need another dashboard. They need a way to capture closed-loop feedback at the moments that matter, surface the themes driving CX performance, and give frontline teams clear priorities without building a data team to interpret it all.

Resonate CX gives banks, insurers, and wealth managers the infrastructure to do exactly that. Feedback is captured across channels (digital, branch, call centre) routed to the right teams, and tracked through to resolution.

Risk Radar flags emerging service failures before they escalate. Robyn AI tells you why scores are moving, not just that they are. And CX Benchmarking shows you how your performance stacks up against industry peers.

For CX managers, the value is in the themes underneath the scores, showing where friction concentrates by product, branch, or interaction type, and giving teams the insights to act on it. Fast.

Frequently Asked Questions

What is customer experience in banking?

Customer experience in banking refers to the full set of interactions a customer has with a financial institution, from onboarding to daily transactions, complaints handling, and product renewals. It spans digital channels, branch interactions, call centres, and everything in between. Strong banking CX reduces churn, drives referrals, and supports regulatory compliance.

How do you improve customer experience in banking?

The highest-impact starting points are fixing the channel handoff (ensuring customers never have to repeat themselves), investing in proactive communication (alerting customers to issues before they need to call), and implementing first-contact complaint resolution. Underpinning all of these is a structured Voice of the Customer program that captures feedback at the right moments and routes it to the right teams.

What is a good NPS score for financial services?

NPS benchmarks vary significantly across the sector. Retail banking typically scores in the 20–35 range for major incumbents; insurance often scores lower, particularly where claims experiences are factored in; wealth management tends to score higher, reflecting more personal client relationships. More important than any single number is the direction of change over time, a consistently improving NPS signals that CX investment is working.

What is a Voice of the Customer program in financial services?

A Voice of the Customer program is a structured system for capturing, analysing, and acting on customer feedback across the full customer journey. In financial services, a real VoC program goes beyond a feedback form. It captures structured insights at defined touchpoints, maps them to specific products and business units, and routes actionable insights to frontline teams. It also functions as an early warning system for regulatory and compliance risk.

How does NPS differ from customer effort score in financial services?

NPS measures the likelihood of a customer recommending an organisation and works best as a relationship-level metric. Customer effort score (CES) measures how much effort a customer had to exert to complete a specific interaction, and is particularly useful for diagnosing friction points in banking and insurance workflows. The most effective CX programs in financial services use both alongside complaint data and operational metrics.